First-Time Homebuyer Guide to Oakville & the GTA (2026): Grants, Programs & Incentives | The Furtado Group

First-Time Homebuyer Guide to Oakville & the GTA (2026): Down Payment Programs, Grants & Incentives

Buying your first home in Oakville or the Greater Toronto Area can feel overwhelming. Between rising prices, competitive offers, and confusing paperwork, it’s easy to miss the financial programs designed specifically for first-time buyers.

Here’s the part most people don’t realize: there can be tens of thousands of dollars in rebates, credits, and tax-advantaged savings available to you if you know what applies (and when to use it).

This guide breaks down the main first-time homebuyer programs available in 2025, including:

- Federal savings tools you can use for a down payment (FHSA + RRSP Home Buyers’ Plan)

- Ontario and Toronto land transfer tax rebates (where applicable)

- New-build GST/HST rebate basics

- A simple “stacking strategy” to maximize benefits

- A checklist you can use before you write your first offer

If you’re still exploring the move itself, start here first:

Moving to Oakville (Neighbourhoods, schools, commute, costs)

https://www.thefurtadogroup.com/blog/Moving-to-Oakville--Ontario--The-Local-Guide-to-Neighbourhoods--Schools--Commute---Costs--2026-

Quick Answer (Featured Snippet)

First-time buyers in Oakville and the GTA often use the First Home Savings Account (FHSA) to build tax-deductible savings and withdraw tax-free for a home purchase, plus the RRSP Home Buyers’ Plan (HBP) to withdraw up to $60,000 per person from RRSPs (tax-free upfront, then repaid over time). At closing, Ontario first-time buyers may qualify for up to a $4,000 land transfer tax rebate, and Toronto buyers may qualify for an additional municipal rebate up to $4,475. New-build purchases may qualify for GST/HST new housing rebates depending on price and structure.

Table of Contents

1) Federal Programs for First-Time Buyers (FHSA + HBP + Home Buyers’ Amount Tax Credit)

2) Land Transfer Tax Rebates (Ontario + Toronto)

3) New Construction: GST/HST New Housing Rebate (What to Know)

4) Down Payment Rules in Canada (How Much You Actually Need)

5) Eligibility: Who Counts as a “First-Time Buyer” (Program-by-Program)

6) The Stacking Strategy (How Buyers Combine Programs)

7) Common Mistakes We See First-Time Buyers Make (Especially in Oakville)

8) First-Time Buyer Checklist (12 months → offer day → after closing)

9) FAQs

10) Next Steps

11) External Sources

Why this guide is written differently (Oakville-first)

We work with first-time buyers across Oakville and the GTA every day. What we see over and over isn’t that programs don’t exist, it’s buyers missing them, misusing them, or learning too late that they qualified.

Oakville is a higher-price market, which means down payment structure, closing costs, and “all-in monthly cost” planning matters even more. This guide is designed to help you make confident decisions before you get emotionally attached to a listing.

If you want a buyer roadmap built for Oakville specifically, grab this too:

Free Buyer’s Guide

https://www.thefurtadogroup.com/free-buyers-guide

Federal Programs for First-Time Buyers (The Ones that Matter Most)

1) First Home Savings Account (FHSA)

The FHSA is one of the most powerful tools for first-time buyers because it combines:

- Tax-deductible contributions (like an RRSP)

- Tax-free withdrawals for a qualifying home purchase (like a TFSA)

How it works (high level):

- Annual contribution room: up to $8,000

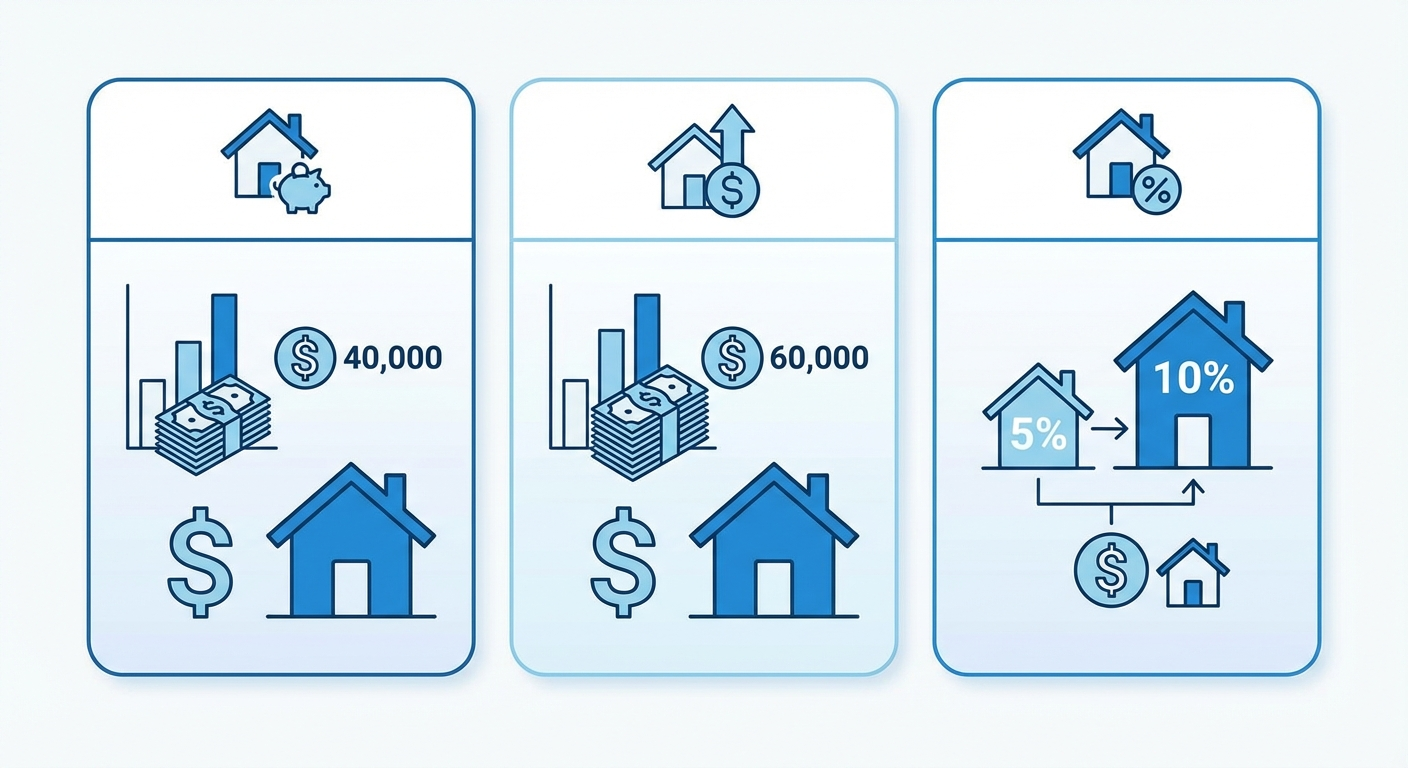

- Lifetime limit: up to $40,000

- Contributions may reduce your taxable income

- Qualifying withdrawals for a first home are tax-free

Quick takeaway: FHSA for Oakville buyers

In Oakville, the FHSA can matter even more because down payments are often larger than the national average. Opening the account early can be a major advantage — even if you only contribute a small amount at first.

Official FHSA details:

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/first-home-savings-account.html

2) RRSP Home Buyers’ Plan (HBP)

The Home Buyers’ Plan lets you withdraw from your RRSP to buy or build a qualifying home:

- Up to $60,000 per person

- Up to $120,000 combined for couples (if both qualify)

- Withdrawals are not taxed at the time of withdrawal

- Repayments are required over time (or missed repayments become taxable income)

Important timing rule:

- RRSP funds generally need to be in the RRSP for at least 90 days before withdrawal eligibility.

Official HBP details:

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/rrsps-related-plans/what-home-buyers-plan.html

3) Home Buyers’ Amount (First-Time Home Buyers’ Tax Credit)

This one doesn’t help with your down payment, but it can reduce your federal taxes owing after you buy.

- The credit is based on an eligible amount of up to $10,000

- The maximum federal tax reduction is up to $1,500 (15% of $10,000)

Important 2025 update: The First-Time Home Buyer Incentive (FTHBI) is discontinued

You may see older articles referencing the shared-equity “First-Time Home Buyer Incentive” (FTHBI). That program has been discontinued and is no longer available for new applications.

In 2025, most first-time buyer planning now focuses on:

- FHSA

- RRSP Home Buyers’ Plan

- Land transfer tax rebates (where applicable)

- Mortgage strategy (approval strength + affordability)

(If you already used the FTHBI in the past, you still need to follow its repayment rules.)

Land Transfer Tax Rebates (Ontario + Toronto)

Ontario Land Transfer Tax Rebate (Up to $4,000)

When you buy property in Ontario, you pay land transfer tax based on the purchase price. First-time buyers may qualify for a refund of up to $4,000.

Key eligibility notes (Ontario):

- You must be at least 18

- Canadian citizen or permanent resident

- You cannot have owned a home (anywhere in the world) before

- Your spouse also cannot have owned a home anywhere in the world while they were your spouse

- You must occupy the home as your principal residence within the required timeline

Official Ontario rules:

https://www.ontario.ca/document/land-transfer-tax/land-transfer-tax-refunds-first-time-homebuyers

Oakville tip: In many cases, buying in Oakville means you avoid Toronto’s additional municipal land transfer tax, which can lower closing costs compared to Toronto purchases.

Toronto Municipal Land Transfer Tax Rebate (Up to $4,475)

If you buy within the City of Toronto, there’s an additional municipal land transfer tax, and first-time buyers may qualify for a rebate up to $4,475.

Official City of Toronto rebate details:

https://www.toronto.ca/services-payments/property-taxes-utilities/municipal-land-transfer-tax-mltt/municipal-land-transfer-tax-mltt-rebate-opportunities/

New Construction: GST/HST New Housing Rebate (What to know)

If you’re buying a newly built home (or substantially renovated), you may be eligible for GST/HST new housing rebates depending on purchase price and how the deal is structured.

Important notes:

- In many new-build transactions, the rebate is already factored into the price and assigned to the builder.

- Always verify how the rebate is treated in the Agreement of Purchase and Sale.

Official CRA overview:

https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/rc4028/gst-hst-new-housing-rebate.html

How much down payment do you actually need in Canada?

Minimum down payment rules are based on the purchase price:

- Up to $500,000: 5%

- $500,001 to $999,999: 5% on the first $500,000 + 10% on the remainder

- $1,000,000+: 20%

Example: $800,000 purchase

- 5% of $500,000 = $25,000

- 10% of $300,000 = $30,000

Minimum down payment = $55,000If you put less than 20% down, you’ll typically need mortgage default insurance (often referred to as “CMHC insurance”), and the premium is usually added to the mortgage amount.

Official CMHC premium info:

https://www.cmhc-schl.gc.ca/professionals/project-funding-and-mortgage-financing/mortgage-loan-insurance/mortgage-loan-insurance-homeownership-programs/premium-information-for-homeowner-and-small-rental-loans

First-time buyer eligibility: do you qualify?

Different programs define “first-time” differently. Here’s the simplest way to think about it:

Federal programs (FHSA + HBP):

- Often based on whether you owned and lived in a home as your principal residence in a recent multi-year window.

Ontario/Toronto land transfer tax rebates:

- Stricter “never owned anywhere in the world” rule (and spouse history matters too).

If you’re not sure, it’s worth verifying before you write an offer — because it can affect your closing cost plan.

If you’re buying in Oakville and want to understand how schools and boundaries affect neighbourhood choice:

Oakville School Zones & Catchment Guide

https://www.thefurtadogroup.com/blog/Oakville-School-Zones---Catchment-Guide--2026---Find-Your-School-by-Address---Neighbourhood-Tips

Maximizing your benefits: the stacking strategy (Oakville-first)

Smart first-time buyers combine programs.

Example strategy (common for Oakville/GTA buyers):

1) Open FHSA early (room starts when the account is opened)

2) Contribute consistently (even small amounts)

3) Use RRSP contributions strategically if planning to use the HBP (watch the 90-day timing rule)

4) Plan closing costs and land transfer tax properly (Ontario rebate; Toronto rebate if applicable)

5) Keep your “offer-day” plan clean: financing confidence + deposit readiness + conditions aligned to risk

Oakville-specific reality:

In Oakville, where many entry-level towns and freeholds can price higher than expected, stacking FHSA savings + HBP funds can be the difference between buying comfortably and stretching too far.

To pressure-test your monthly “all-in” reality, this post helps:

Cost of Living in Oakville

https://www.thefurtadogroup.com/blog/cost-of-living-in-oakville-ontario

Common mistakes first-time buyers make (especially in Oakville)

1) Waiting too long to open an FHSA

FHSA room starts when the account opens — not years before. Opening early can matter.

2) Missing the RRSP 90-day rule for HBP

Last-minute RRSP contributions can fail the timing requirement.

3) Underestimating closing costs

Even with rebates, you should plan for legal fees, title insurance, inspections, moving costs, and “day-one” expenses.

4) Only comparing homes by price (not all-in monthly cost)

Mortgage payment is only part of the story. Taxes, utilities, commute, and fees can change the real monthly number.

If commuting is part of your decision, read this:

Commuting from Oakville to Toronto (GO train, parking, fares, commuter neighbourhoods)

https://www.thefurtadogroup.com/blog/Commuting-from-Oakville-to-Toronto--2026---GO-Train-Times--Parking--Fares---Best-Neighbourhoods-for-Commuters

5) Skipping home inspections without a risk plan

In a competitive market, some buyers waive conditions. If you do, make sure you understand the trade-off.

6) Assuming you don’t qualify

Some buyers qualify federally but not provincially (or vice versa). Always confirm program-by-program.

First-time buyer checklist (12 months → offer day → after closing)

12+ months before buying

- Open an FHSA (even if you start small)

- Build your down payment plan (FHSA + savings + RRSP strategy if using HBP)

- Check credit and address issues early

- Start learning neighbourhoods and your non-negotiables

3–6 months before buying

- Get a mortgage pre-approval (and understand your realistic payment range)

- Build a closing cost plan (land transfer tax, legal, inspection, moving)

- Shortlist neighbourhoods (schools/commute/lifestyle)

When making an offer

- Confirm which programs apply to your situation

- Confirm deposit requirements and timing

- Decide which conditions are essential (financing, inspection, status cert for condos)

After closing

- Track HBP repayment schedule (if used)

- Keep program documentation for tax season

- Update address and services

FAQs (AI + Featured Snippet Optimized)

Can I use the FHSA and RRSP Home Buyers’ Plan together?

Yes. Many first-time buyers use both. You can withdraw qualifying FHSA funds tax-free and also use the HBP for RRSP withdrawals (with repayment requirements).

Do these programs apply to condos?

Yes, generally. Condos, towns, and detached homes can qualify as long as the home will be your principal residence and you meet the program rules.

What if my spouse owned a home before?

It depends on the program. Some federal programs focus on your recent principal residence history, while Ontario/Toronto land transfer tax rebates have strict rules that consider spouse ownership history. Confirm before closing.

What happens if I don’t buy a home after opening an FHSA?

You can keep it open (subject to program rules) and may be able to transfer funds to an RRSP rather than withdrawing as taxable income. Confirm the latest rules with CRA.

Is the First-Time Home Buyer Incentive still available?

No. The shared-equity First-Time Home Buyer Incentive (FTHBI) has been discontinued for new applications.

Next steps:

If you’re buying your first home in Oakville or the GTA, the most valuable next step is understanding what programs actually apply to your situation — and building a clean plan before offer day.

If you want a no-pressure walkthrough, start here:

Buy With Us

https://www.thefurtadogroup.com/buy-with-us

Or learn more about the team:

About The Furtado Group

https://www.thefurtadogroup.com/about

Last updated: 2025

Disclaimer: This guide is for informational purposes only and does not constitute legal, tax, or financial advice. Program details and eligibility can change. Always verify current terms with official government sources and qualified professionals.

External Sources (Official Links)

Home Buyers’ Plan (CRA)

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/rrsps-related-plans/what-home-buyers-plan.html

Home Buyers’ Amount (CRA)

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/about-your-tax-return/tax-return/completing-a-tax-return/deductions-credits-expenses/line-31270-home-buyers-amount.html

Ontario Land Transfer Tax Refund (Ontario.ca)

https://www.ontario.ca/document/land-transfer-tax/land-transfer-tax-refunds-first-time-homebuyers

Toronto MLTT Rebate (City of Toronto)

https://www.toronto.ca/services-payments/property-taxes-utilities/municipal-land-transfer-tax-mltt/municipal-land-transfer-tax-mltt-rebate-opportunities/

GST/HST New Housing Rebate (CRA)

https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/rc4028/gst-hst-new-housing-rebate.html

CMHC Mortgage Loan Insurance Premium Info

https://www.cmhc-schl.gc.ca/professionals/project-funding-and-mortgage-financing/mortgage-loan-insurance/mortgage-loan-insurance-homeownership-programs/premium-information-for-homeowner-and-small-rental-loans

Categories

Recent Posts